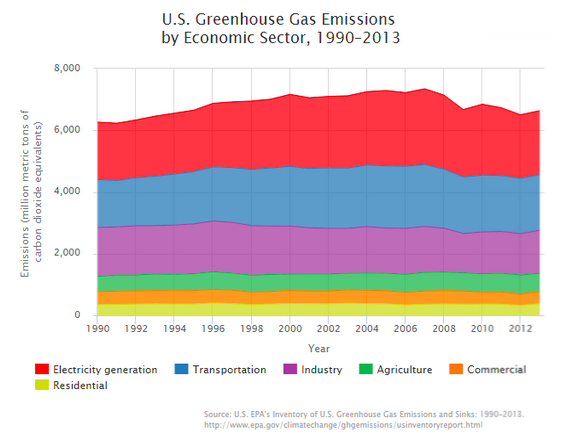

Last week President Obama, in conjunction with the EPA, introduced the final rule of the Clean Power Plan. The plan targets the power generation sector which currently accounts for roughly a third of the nation’s greenhouse gas emissions. Much of current regulations limit emissions of soot and other toxic byproducts of fossil fuel combustion. The CPP sets aggressive yet achievable standards to reduce CO2 from generators by 32% from 2005 levels by 2030.

Although the current CPP iteration constitutes a slightly more aggressive cut in emissions, the plan affords individual states the luxury of determining their own path to compliance. The CPP ultimately stands to incentivize all low-carbon electricity generation technologies including solar, energy efficiency measures, natural gas, nuclear and carbon capture and storage requiring renewables account for 28% of generation mix. Furthermore the plan offers opportunities for states to opt in to emission credits trading markets.

What does the CPP mean for solar? Will the CPP increase solar development above usual rates of capacity addition? The extent of solar expansion driven by the CPP will ultimately be determined by the plan each state adopts to meet its reduction target. For example a state may decide to achieve it target through gains in efficiency paired with new gas-fired combined cycle natural gas turbines. Another state may rely on solar to meets its target. Available sun hours and irradiance of different regions will also play a role in the rate of solar expansion.

The strategy that each state chooses to employ will depend upon a wide spectrum of factors. States with favorable solar policy may be inclined to meet a significant portion of their target through increased PV capacity. These states may also be home to electricity rates above the national average, further promoting the use of solar to lower emissions. Conversely, states like Washington where roughly 50% of electricity comes from hydro and rates are low may opt to improve the efficiency of existing fossil plants to stay on target.

The CPP also invigorates the opportunity to renew the solar Investment Tax Credit (ITC), currently slated to drop from 30% to 10% at the close of 2016. Legislators may find it wise to extend or modify the ITC step-down to coincide with capacity reductions brought by the CPP. Paired with the EPA Clean Energy Incentive Program, which encourages early adoption of renewable sources of energy, these policy mechanisms will serve to promote rapid growth in solar and other renewable generator capacity.

The latest iteration of the CPP has spurred much conversation surrounding the potential for job growth and loss. As with most debates surrounding job growth, figures vary by state and industry affiliation. What is clear, however, is that the CPP is likely to serve as a catalyst for significant job creation in solar and other renewables both up and downstream in the US.